by senior futurist Richard Worzel, C.F.A.

“The market can remain irrational longer than you can remain solvent.”

– John Maynard Keynes *

The U.S. stock market has been on one of the great bull market runs in history, more than tripling since the market bottom on March 9th, 2009. And it continues to defy gravity and its critics, echoing Mark Twain’s comment about reports of its death being exaggerated.

But no tree grows all the way to the sky, as a classic market cliché goes, and this market is at or near the top by virtue of almost any measure of value or price. The problem is, as my opening quote cites, that markets can stay irrational for a long time.

So, given this uncertainty, what’s the proper strategy to adopt now?

This is where a futurist’s approach to risk management can be helpful: You don’t have to know the future to be able to plan intelligently for what’s ahead. Instead, you assess the odds, and the potential for risk and reward, then select the option that puts the odds in your favor. Let’s take a look at what that might look like, and what actions it might lead to.

What Is Risk?

I’m a Chartered Financial Analyst, and used to work in the investment industry. I’ve had a long-standing disagreement with many market-oriented quantitative analysts over the definition of risk, and the current market exemplifies this difference.

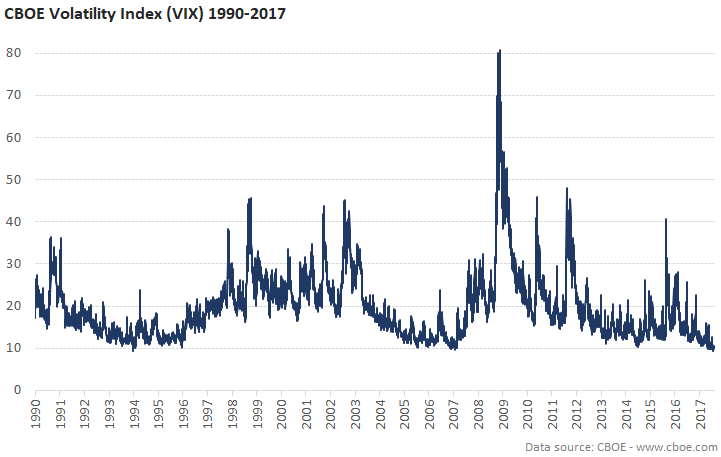

The traditional quant’s definition of risk is volatility: the more volatile an investment is, the riskier it is. Yet, the current market has been surprisingly un-volatile. Indeed, the one of the most broadly used measures of volatility, the Chicago Board of Trade’s Volatility Index, called the VIX, has been remarkably quiet:

Does this lack of volatility mean the current market is not risky? That would be a foolish conclusion as even market bulls concede the market can’t keep going up forever, and that this run has been near-historic in proportion.

My own definition of risk is more real-world obvious: Risk is the cost of being wrong. So, let’s look at how investors could be right, and how they might be wrong, and then try to quantify the risks either way.

Let me start by assuming that I’m wrong about the market. What would be the consequences or cost to me? Well, the obvious one is that the market could continue to go up, but my investment holdings won’t as I have sold most of my stock positions.

How much might I lose? From where it is today, it’s hard to see the market advancing by as much as 10% over the next 12 months, so losing out on an additional 10% is my estimated cost. Moreover, I think that this is being generous in my assessment of how much further the market could run.

Now let’s consider the consequences or costs to an investor who is fully invested, and has an aggressive portfolio of stocks. How much might that cost such a person?

A minor market correction is generally considered to be a decline of about 10%. Such a decline will typically happen once or twice a year during a bull market (but hasn’t happened since February of last year).

A major market correction is generally taken to imply a decline of 25% or more. For comparison, the S&P 500 Index lost almost half its value in the 2007-09 market panic.

So, while I might stand to lose as much as 10% by staying away from stocks, our hypothetical aggressive investor might lose 25% in a run-of-the-mill bear market.

There’s a tool in statistics called Expected Return. To calculate it, you multiply the potential gain by the probability of gain, then add that to the potential loss times the probability of loss. To provide a simplistic illustration, let’s assume that there’s a 50-50 chance of a continuation of the bull market versus the advent of a bear market, that if the market rises, it rises by 10%, and if it falls it falls by 25%:

Expected Return = (50% x 10%) + (50% x -25%)

= +5% – 12.5% = -7.5%

In other words, in this simplistic illustration you should expect to lose 7½% by investing or staying invested. That would not be a smart investment call; you don’t normally buy an investment when you are expecting to lose money on it.

But have I assessed the potential gains and losses properly, and assigned appropriate odds?

What Is This Market’s Expected Return?

There are always pundits saying that markets are cheap, and others saying it’s expensive. Let’s go through a couple of the reasons why I believe this market is expensive.

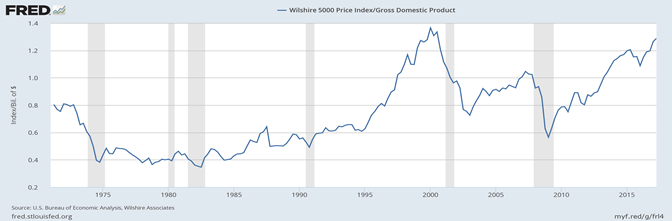

One of the best, long-term ways of valuing a market is to look at the total market capitalization relative to Gross Domestic Product, i.e., the value of the market compared to the value of the overall economy. After all, stocks represent how well the economy is working, so shouldn’t get too far ahead of it.

Fortunately, this yardstick is readily available from FRED, Federal Reserve Bank Economic Data, which is a database maintained by the U.S. Federal Reserve Bank of St. Louis. Here’s what that ratio looks like graphically:

A recent value of this ratio had the market capitalization at 138% of GDP, whereas the 50-year average is 65%. This would mean we would have to have a 53% decline to bring us back to average – and markets almost always overshoot in whichever direction they move.

Another value yardstick that is highly thought of is the Case-Shiller PE Ratio[1], which also indicates that the market is almost historically overvalued:

The only times the Case-Shiller PE has been higher were (a) at the height of the tech boom in December of 1999, and (b) at the height of the stock market boom of the Roaring 20s, just before the Black Tuesday crash of October, 1929.

This indicator is currently 31.62, compared to the long-term mean (average) of 16.80. In other words, it would (coincidentally) have to decline by about 53% to get back to the long-term average.

There are several other indicators that might be relevant, but my point is that the cost of being wrong on the market now would likely be very high. The potential loss would be high by historic standards, perhaps on the order of 50% or more.

What’s the Probability of a Market Collapse?

Now that we’ve looked at the cost, let’s look at the probability of being wrong by considering the environment in which the market is operating. In other words, what and where are developments that might derail the market? (The list below is in no particular order.)

- The potential for a nuclear war with North Korea.

- The potential for war in the Middle East involving Saudi Arabia, which would affect the price of oil, as well increase the instability of Mideastern politics.

- Economic and political conflict between Britain and the EU over Brexit.

- Rising interest rates, and the reduction of quantitative easing by central banks, but especially the U.S. Federal Reserve, leading to a sell-off of bonds and interest-sensitive stocks.

- High levels of corporate and personal indebtedness, which would lead to financial difficulties if the economy slows.

- The earnings of the S&P 500 peaked in the third quarter of 2014, but the market has continued to rise despite disappointing earnings.

- The yield curve is flattening, which is a reflection of rising short-term rates. A flat yield curve is typically a forerunner of an economic slowdown.

- Consumers’ ability to drive the economy is weakening. In a succinct commentary on market conditions by money manager J. Lawrence Manley, Jr. notes that:

“It appears the consumer is struggling. Real wage growth is stagnant, and employment growth is declining. Additionally, the personal savings rate has dropped sharply over the past two years as individuals were forced to reduce their savings rate to fund their consumption. We believe that a significant economic acceleration is unlikely, given the weak fundamentals in the consumer sector of the economy.[2]

- The market is already assuming that significant tax cuts by the Congress and Administration will pass, but this is far from certain. If they don’t pass, the market will be disappointed.

In short, there are lots of things that threaten this bull market, including the keys: stagnant corporate earnings, eroding consumer spending, rising interest rates, and an aging economic boom.

And yet, market psychology remains buoyant, and markets continue to roll merrily along, acting as if everything is not only great, but getting better. That’s not the case. And from my perspective, this means that the risks are high and rising that the market will roll over.

I would estimate that the odds of the market turning down over the next 12 months are between 70-80%. Let’s pick 75% as a point estimate. This means that I would peg the odds of the market continuing to rise at 25%, coupled with my earlier estimate of the potential for missed gain is about 10%.

Plugging these figures into the Expected Return formula gives:

Expected Return = (25% x 10%) + (75% x -50%)

= +2.5% – 37.5%

= –35%

In other words, I expect that an investment made (or kept!) in the broad U.S. stock market would lose 35% of its value over the next year.

Clearly, this is a high-risk bet. The cost of being wrong, and the probability of being wrong are both high.

Nobody Knows When a Market Will Turn

Do I know when the market will stop going up and turn down? No; no one does. But I think the risks clearly outweigh the potential returns. I could be wrong, and there are undoubtedly plenty of people who will think so.

But step back and consider the probabilities of the bull market continuing up versus seeing the market crumble and fall into bear territory, and think about what your risk is either way.

How much might you miss by being out of the market?

How much might you lose by staying in?

Which risk is greater?

© Copyright, IF Research, November 2017.

• There is some controversy about who said this. Keynes is usually credited with saying it, but it has also been attributed to economist A. Gary Shilling. See, for instance, https://www.maynardkeynes.org/keynes-the-speculator.html

[1] http://www.multpl.com/shiller-pe/

[2] “The Financial Asset Bubble Is Ending”, https://seekingalpha.com/article/4116560-financial-asset-bubble-ending-time-re-examine-risk-allocation